📉 From Globalization to Fragmentation

Global growth is slowing to 3.2 percent in 2025 and 3.1 percent in 2026. Inflation is easing but unevenly. And the world economy is entering a phase defined by fragmentation, trade barriers, and technological reshoring.

While policymakers debate tariffs and fiscal buffers, another transformation is unfolding silently in the background the rewiring of money itself.

As supply chains realign, payment chains are evolving too. Cross-border settlements, correspondent banking flows, and corporate liquidity networks are all being challenged by the same forces reshaping global trade.

In this blog, I explore what the IMF’s macroeconomic diagnosis means for the future of payments and why the next decade will belong to those who build resilient, interoperable, and policy-aware digital money rails.

🏦 IMF 2025: A World of Slow Growth and Fast Money

According to the IMF, advanced economies will hover around 1.5% growth, while emerging markets maintain just above 4%. But beneath those averages lies a tectonic shift:

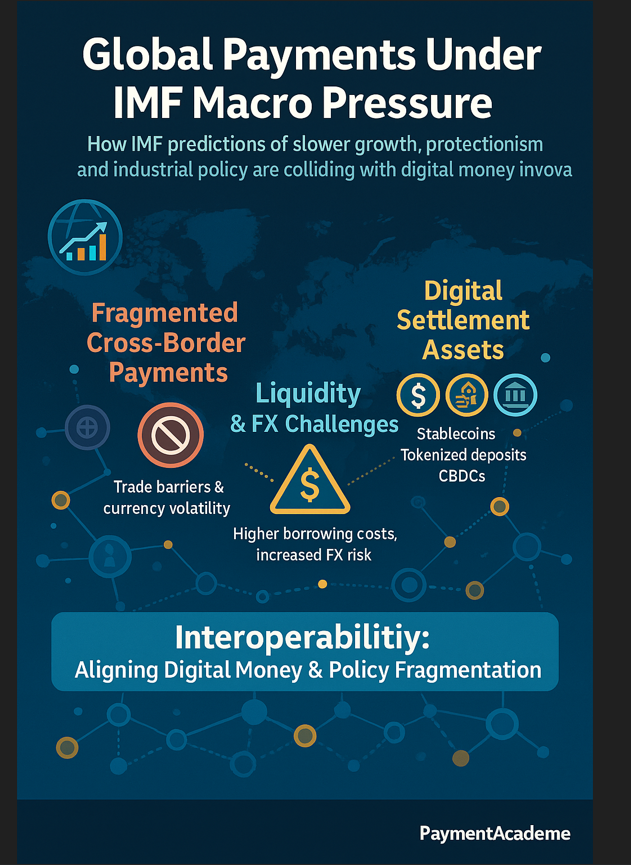

- Protectionism & Policy Volatility: Tariff wars and industrial subsidies are creating currency and capital flow fragmentation.

- Fiscal Vulnerability: Higher borrowing costs are pressuring sovereigns and banks alike, raising the cost of liquidity.

- Monetary Divergence: While some central banks still fight inflation, others prepare for easing creating FX volatility and settlement timing gaps.

In short: money is no longer synchronized.

Global payments are caught between slow-moving policy and fast-evolving technology.

💹 Emerging Markets: Resilience Built on Digital Infrastructure

Chapter 2 of the IMF report “Emerging Market Resilience: Good Luck or Good Policies?” deserves attention from every payments leader.

Emerging markets weathered recent shocks because they improved monetary and fiscal credibility, reduced FX interventions, and built more autonomous financial systems.

That resilience is now extending to digital financial infrastructure:

- Central banks in Brazil, India, and Indonesia are deploying 24/7 instant payment rails with interoperability standards.

- Regional schemes like Singapore’s PayNow + PromptPay and India’s UPI link are proving that emerging markets can leapfrog legacy systems.

- Many are integrating stablecoins or tokenized deposits within sandbox environments to manage cross-border liquidity.

The IMF notes that policy credibility reduces the need for FX interventions. In payments, tokenization does the same reducing friction by making value movements self-verifiable and settlement finality instant.

🔄 Industrial Policy and the New Payment Geography

Chapter 3 of the WEO — “Industrial Policy: Managing Trade-Offs to Promote Growth and Resilience” warns that onshoring and subsidy races could distort resource allocation.

In payments, the parallel is clear: fragmented domestic initiatives can create digital payment silos.

Each region wants its own CBDC, its own stablecoin standards, and its own instant payment rails.

The risk is that we end up with islands of innovation that don’t speak to each other.

Yet industrial policy also offers a new opportunity: it can align strategic payments infrastructure with trade objectives.

If energy security is a priority, then cross-border settlement for commodities should run on programmable, auditable ledgers that reduce counterparty risk.

If manufacturing is being onshored, supply-chain financing should leverage tokenized invoices to speed capital recycling.

Industrial policy without payments modernization is like building highways without toll lanes movement exists, but value capture doesn’t.

🪙 The Rise of Digital Settlement Assets

Against this macro backdrop, stablecoins and tokenized deposits are emerging as the new mediums of trust.

- Stablecoins (USDC, EUROD, JPYC) offer cross-border speed and dollar access but face regulatory arbitrage.

- Tokenized deposits stay within bank balance sheets, aligning with prudential rules while modernizing infrastructure.

- Wholesale CBDCs provide inter-bank settlement finality under central-bank supervision.

In a world where growth is slowing and debt is rising, these models represent the search for efficiency and control. They allow faster settlement with lower liquidity costs, reducing the working-capital drag that plagues global supply chains.

💡 Macro Implications for Global Payments Players

- Liquidity Becomes a Competitive Edge

In a low-growth world, banks and fintechs that can offer real-time cross-currency settlement gain a decisive advantage. Static cash trapped in nostro accounts is a costly luxury. - Monetary Divergence Drives FX Innovation

With rates diverging, corporates will seek FX-hedged stablecoin solutions that automate conversion and settlement. - Risk Repricing Fuels RegTech Integration

The IMF’s warning about financial market fragilities will accelerate demand for tokenized audit trails and real-time transaction monitoring. - Policy Pressure Pushes for Interoperability

Fragmented standards could hinder global flows. The next phase of innovation will be led by players who can bridge CBDCs, stablecoins, and RTGS systems seamlessly. - Cross-Border Resilience Becomes the New Metric

The question is no longer “how fast is your rail?” but “how resilient is your liquidity under policy shock?”

🔗 Interoperability: From Ideal to Imperative

The IMF urges countries to preserve institutional credibility and restore confidence through transparent policy.

In payments, the equivalent is restoring trust through interoperability.

- Technological interoperability (connecting token networks and legacy rails)

- Regulatory interoperability (mutual recognition of digital-asset frameworks)

- Data interoperability (standardized reporting for risk and compliance)

Without these, fragmentation will be the default.

With them, we get a globally cohesive digital payment architecture a foundation for inclusive growth even in a low-growth world.

🧭 A Framework for Policy Aligned Payments

To align with the IMF’s macro objectives stability, transparency, sustainability payment architects must build on four principles:

- Programmable Transparency – Use smart contracts and on-chain audit trails to enhance policy monitoring.

- Liquidity Circularity – Re-use tokenized liquidity across corridors instead of trapping funds locally.

- Policy-Anchored Innovation – Engage regulators early; design for compliance from day zero.

- Cross-Sector Integration – Link payments to trade, logistics, and energy flows to support industrial policy goals.

This approach creates a payments ecosystem that is not just fast but macroeconomically resilient.

⚙️ 2026 and Beyond: Re-Imagining Global Payments Through Policy Lenses

As the IMF warns of dim prospects for growth, payments become a lever for productivity.

Reducing settlement latency and FX costs can add basis-points of GDP — a rare form of policy alpha when monetary and fiscal tools are constrained.

In this context, central banks and transaction banks must collaborate on a shared vision:

A global payment infrastructure that moves value as freely as information, while preserving the stability of the financial system.

That balance speed without speculation, innovation without instability will define the next decade of monetary innovation.

✍️ Final Thoughts

The IMF calls for credible, transparent, and sustainable policies. In payments, that translates to programmable trust.

Every cross-border payment is a policy event — it moves capital, signals confidence, and reflects institutional strength.

Stablecoins, tokenized deposits, and CBDCs are not detached from the IMF’s macro agenda, they are its technological continuation.

The next frontier in payments won’t be about speed or UI design. It’ll be about resilience, policy alignment, and programmable transparency. When inflation is volatile, liquidity fragmented, and regulation uneven, the payment systems that win will be those anchored in macro trust — yet flexible enough to operate in a decentralized world.

Central banks are setting frameworks. Commercial banks are testing tokenized deposits. Fintechs are building settlement layers that run 24/7. Together, they’re converging toward a single outcome:

Money that moves with policy discipline, but at digital speed.

That’s the architecture of the future one where compliance is embedded in code, liquidity moves without friction, and every transaction reinforces systemic stability rather than testing it.